发布时间: 2016.06.01

文章作者:

您现在的位置:楷柏财经首页>

ACCA F3重难点解析——9个case帮你理清F3重难点!

自从F3实行机考后, 考前猜题变得毫无意义。楷博财经现将教学过程中, 同学们遇到的部分重难点做出解析。

Case 1

Erin is registered for sales tax.During May, she sells goods with a tax exclusive price of $600 to Kyle oncredit. As Kyle is buying a large quantity of goods, Erin reduces the price by5%. She also offers a discount of another 3% if Kyle pays within 10 days. Kyledoes not pay within the 10 days. If sales tax is charged at 17.5%, what amountshould Erin charge on this transaction?

解析

信用交易发生的时点,卖方要开具销售发票,此时会有一个假设: 买方会在10天内支付货款,从而得到early discount (3%)

因此,此交易产生的销项税为 $600 X 95% X 97% X 17.5%

如果买方在10天后才支付,需要补开一张发票,票面销项税为 $600 X 95% X 3% X 17.5%

Case 2

解析

在采购价格一直上涨的背景下(i.e.inflation), 公司使用3种Valuation methods, 对Cost of sales, profit and closing inventory value 的影响总结如上. 英文表述如下:

During inflationary period, FIFO gives the highestclosing value and profit, but lowest COS;

During inflationary period, LIFO gives the lowest closingvalue and profit, but highest COS;

AVCO always stand in the middle.

Case 3

Chapter 6 Inventory 中2个"特殊"会计分录

(1)Owner 拿公司存货自用

Dr. Equity (所有者权益减少)

Cr. Inventory drawing (or Purchase or COS) (COS减少)

(2)拿公司存货作为固定资产使用,如电脑

Dr. Non-current asset (固定资产增加)

Cr. COS (or Purchase ) (期间采购成本减少或COS减少)

解析

国际会计准则下,公司对期间存货增加或减少不会记录在会计系统中的Ledger account (i.e. Inventory ledgeraccount), 即如下会计分录是错误的:

Dr. Inventory

Cr. Payables or cash

我们将期间采购(赊购或现金采购) 行为视为"采购费用"的发生 , 即:

Dr. Purchase

Cr. Payables or cash

也就是说,期间存货减少, 我们不能贷记Inventory.

Case 4

Chapter 10 的年末调整分录,对P&L and B/S的影响如下:

Chapter 11

On 1 January 2013 Tipton’s trade receivables were $10,000. The followingrelates to the year ended 31 December 2013:

Credit sales $100,000

Cash receipts $90,000

Discounts allowed $800

Discounts received $700

Cash receiptsinclude $1,000 in respect of a receivable previously written off. Calculate theclosing value of receivable:

解析

Method 1:

The closingbalance = Opening + Addition – Receipts – Discount + bad debts recovered

= 10,000+ 100,000 – 90,000 – 800 + 1,000

Note: Discountreceived has nothing to do with salesor TR

Method 2:

Note 1: 期间从信用客户收到$90,000其中$1,000 之前已经作为坏账write off, 现在收到了这笔钱,不能视为Receivable的减少. 参见下面的分录:

1.Cash received | |

Dr Irrecoverable debts 1,000 | Dr Bank 1,000 |

Cr TR 1,000 | Cr Irrecoverable debts 1,000 |

Method 3:

之前将之write off | 随后客户通知准备还钱 | 真正收到钱 |

Dr Irrecoverable debts 1,000 | Dr TR 1,000 | Dr Bank 1,000 |

Cr TR 1,000 | Cr Irrecoverable debts 1,000 | Cr TR 1,000 |

Note: Method 2 and 3的区别在于: method 2 没有做中间的分录

Case 6

Chapter 12 Provision and contingentliability

IAS 37 requires contingent liabilities and assets are summarized inthe following table:

Probability of Occurrence | Liabilities | Assets |

Virtually certain (>95%) | Recognize (确认为负债 如TP) | Recognize (确认为资产 如TR) |

Probable (51% - 95%) | Provide and disclose in note | Disclose in note |

Possible = not likely (5% -50%) | Disclose in note | Ignore |

Remote (< 5%) | Ignore | Ignore |

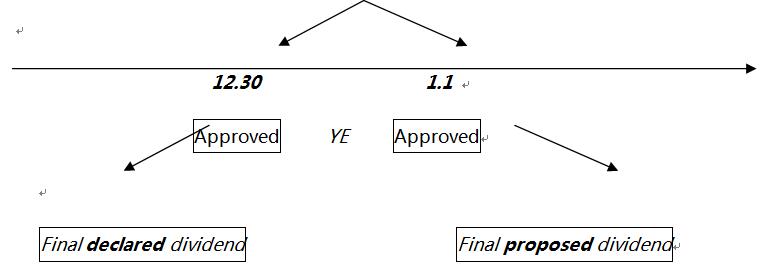

Case 7

Chapter 13 Capital structure

| Approving body | Accounting entries |

Mid-year / interim dividend | Board of directors | Dr Retained Earnings - Dividends Cr Bank (B/S) |

Final dividend | Annual General Meeting (AGM) | Dr Retained Earnings - Dividends Cr Dividends payable (B/S) |

解析

年末对普通股股东分红,需得到股东大会的批准. 得到批准的时点很重要,如果是年末前得到Approval, 则叫做Final declared dividend; 年后得到Approval,则Final proposed dividend. 对于2种情况的会计处理如上。

Case 8

Chapter 13 Capital structure

Corporation tax

Over-provision | Under-provision |

2015.12.31 Estimate tax for 2015 1Dr Tax Charge $1,000 Cr Tax payable $1,000 对2015年应纳税金作出预估 | 2015.12.31 Estimate tax for 2015 1Dr Tax Charge $1,000 Cr Tax payable $1,000 对2015年应纳税金作出预估 |

2016.2.2 Taxman collects the tax 2Dr Tax Payable $800 Cr Bank $800 源于年末多提, 实际比预估少200(Over-provision) 导致Tax Payable贷方余额200 | 2016.2.2 Taxman collects the tax 2Dr Tax Payable $1,200 Cr Bank $1,200 源于年末少提, 实际比预估多200 (Under-provision) 导致Tax Payable借方余额200 |

2016.12.31 本期已经付清属于去年的税金, 因此对Tax Payable科目贷方余额调整: YE Adjustment 3Dr Tax payable $200 Cr Tax charge $200 后果: 导致2016年计入P&L的tax charge______ 导致2016年tax payable 余额 = ________ | 2016.12.31 本期已经付清属于去年的税金, 因此对Tax Payable科目借方余额作出调整: YE Adjustment 3Dr Tax charge $200 Cr Tax payable $200 导致2016年计入P&L的 tax charge _______ 导致2016年tax payable 余额 = ________ |

1 + 2 + 3 = Dr Tax charge $800 Cr Bank $800 | 1 + 2 + 3 = Dr Tax charge $1,200 Cr Bank $1,200 |

解析

上述故事, 源自公司去年年末对去年税费预提时,出现了多提或少提的情况.

因此我们在本年年末,做出 3 的调整分录.

Case 9

Chapter 17 Preparing financialstatement

Double entry | Impact | Chapter | |

Opening inventory | Dr Cost of sales Cr Inventory | P&L B/S | 6 |

Closing inventory | Dr Inventory Cr Cost of sales | B/S P&L | 6 |

Depreciation charge for the year | Dr Depreciation expense Cr Accumulated depreciation | P&L B/S | 7 |

Accruals and prepayment | 参见Case 4 |

| 10 |

Irrecoverable debts | Dr Irrecoverable expense Cr Receivables | P&L B/S | 11 |

Allowance for receivables | Increase in allowance: Dr Irrecoverable debt Cr Allowance for receivable Decrease in allowance: Dr Allowance for receivable Cr Irrecoverable debt expense |

P&L B/S

B/S P&L |

11 |

Tax estimate for the year | Dr Tax charge Cr Current tax liabilities | P&L B/S |

13 |

Adjustments for prior year's tax estimates | Over-provision in prior year: Dr Current tax provision Cr Tax charge for this year Under-provision in prior year: Dr Tax charge for this year Cr Current tax provision |

B/S P&L

P&L B/S |

(图10)

解析

在17章编制财务报表过程中,有很多年末调整事项. 以上总结了这些调整事项. 注意每个调整分录,影响的是2个不同的主表: P&L or Balance sheet.

以上就是楷博财经对F3的9个经典题型的解析,希望同学们在考试中,能够举一反三,最后能在考试中取得优异的成绩。

发布时间: 2016.06.01

文章作者: